Schwab: Slowing Down While Speeding Up

November 13, 2019

Key Points

- U.S. stocks have surged on hopes of a near-term “phase one” trade deal; yet major issues remain unresolved and investor sentiment is getting frothy.

- Upside surprises in payrolls have reinforced the strength of the labor market and consumer, underlining the bifurcation within the broader U.S. economy.

- Hints at global fiscal stimulus are starting to manifest themselves in policy plans, signaling a concerted shift away from monetary easing.

Take it to the limit

U.S. stocks have broken out to the upside and surpassed their all-time highs. Recent gains have come on the heels of increased hopes of a signed “phase one” deal by year-end; the Fed’s accommodative rate cut in October; and better-than-expected results from October’s payroll data. Yet, though the past month’s rally has been confirmed by cyclical leadership and relative strength within small-cap and value stocks, caution is warranted; as earnings growth in the third quarter is still expected to be negative year-over-year (as per Refinitiv data), investor sentiment is approaching excessively optimistic levels, and a “skinny” U.S.-China trade deal is unlikely to lift corporate animal spirits. More broadly, U.S. real gross domestic product (GDP) growth estimates for the fourth quarter—as measured by the Atlanta Fed’s GDPNow forecast—have edged down to 1% as of November 5, 2019.

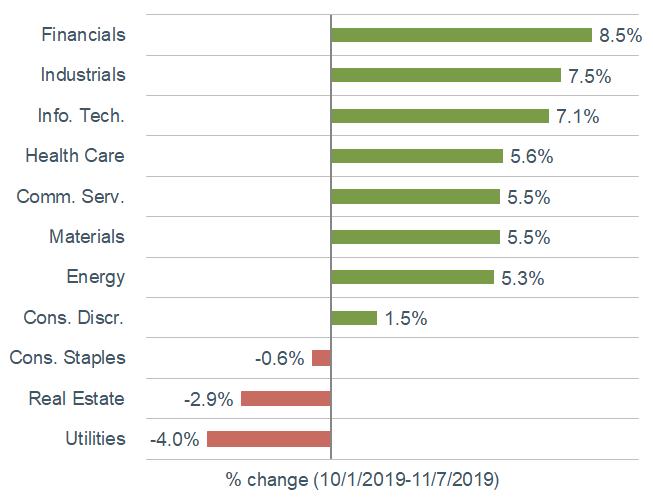

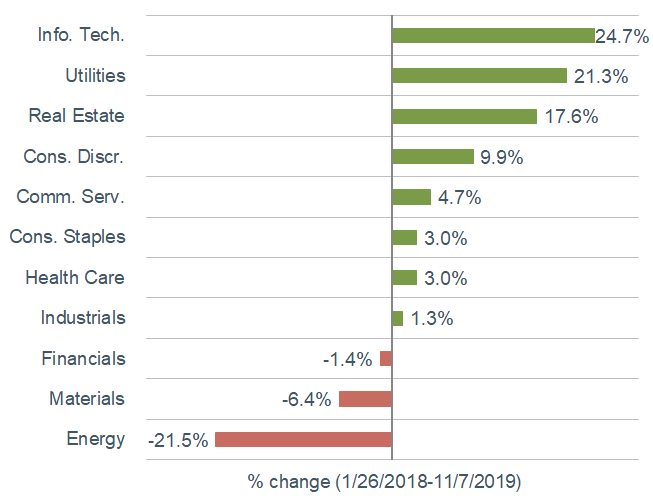

Investors have largely shrugged off various headwinds and embraced riskier areas of the market; yet the reversal hasn’t masked the broader (nearly) two-year defensive trend. You can see from the two charts below that while cyclical sectors have assumed leadership over the past month, they have still lagged their defensive peers over the past 22 months.

Cyclical Sectors Have Led the Recent Market Rally…

Source: Charles Schwab, Bloomberg. For illustrative purposes only. Past performance is no guarantee of future results.

…Yet Defensive Sectors Still Rank Higher Over the Long-Term

Source: Charles Schwab, Bloomberg. For illustrative purposes only. Past performance is no guarantee of future results.

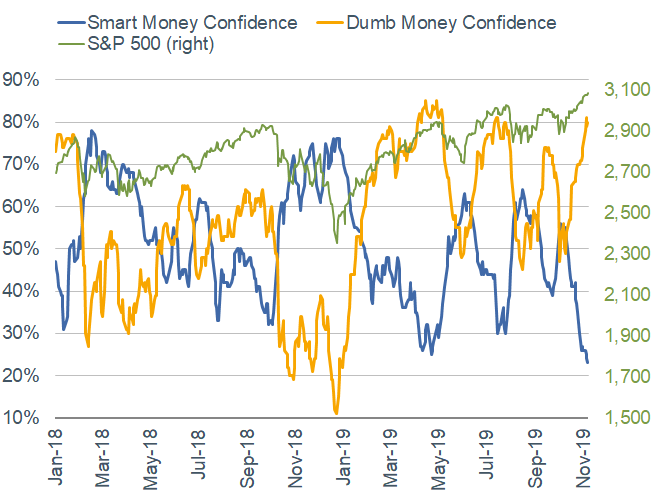

Coinciding with the recent risk-on behavior has been a surge in optimism among various measures of investor sentiment; including one that we track daily—SentimenTrader’s “Smart Money and Dumb Money Confidence” measures. The former cohort consists of institutional and professional investors, while the latter includes smaller odd-lot traders and investors; and they are behavioral measures in that they track how the cohorts are positioned. As you can see in the chart below, “Dumb Money” confidence has surged of late; yet the rub is that, typically at extremes, the “Smart Money” correctly identifies excessive optimism and sniffs out a subsequent market pullback. Should that be the case in the near future, it wouldn’t be all too surprising; considering U.S. stocks have rallied on decreasing uncertainty in the near-term, rather than confidence in longer-term fundamentals.

“Smart Money” and “Dumb Money” Have Diverged Again

Source: Charles Schwab, Sentiment Trader, as of 11/7/2019. Confidence Indexes are presented on a scale of 0% to 100%. When the Smart Money Confidence Index is at 100%, it means that those most correct on market direction are 100% confident of a rising market. When it is at 0%, it means good market timers are 0% confident in a rally. The Dumb Money Confidence Index works in the opposite manner.

Slow versus steady

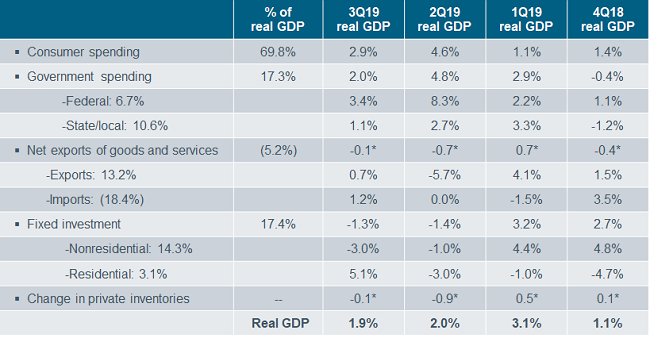

The initial release of third quarter U.S. GDP was 1.9%, which beat the consensus expectation of 1.6%, but was down from 2% in the second quarter. While the headline number reflects moderate growth at best, economic activity has decisively weakened since the beginning of the year. As you can see in the table below, most of the weakness has been concentrated in the business sector (namely, nonresidential fixed investment); while consumer spending has held up fairly well.

Business Spending Has Pulled Growth Down

Source: Charles Schwab, Bureau of Economic Analysis, as of 9/30/2019. *Represents contribution to percent change in real GDP. Numbers may not add up to 100% due to rounding. All components represent annualized quarter/quarter percentage change.

Many pundits have opined that the strength of the consumer has been and will be enough to hold up the U.S. economy, despite myriad uncertainties and an ailing business community. Yet, the reality is that business investment’s ultimate impact carries a lot more heft than its 14.3% weight (measured by the Bureau of Economic Analysis) in overall GDP. In fact, in nearly half of the 41 negative quarters of GDP since World War II, business investment turned negative while personal consumption stayed positive. Thus, even if the consumer remains solid in the near future, it doesn’t necessarily portend a meaningful rebound in growth if business investment continues to wane. There are high correlations among business confidence, corporate profits, capital spending and ultimately job growth. Those are the transmission mechanisms on which to keep a close eye. For now though, the dividing line between business and consumer confidence remains firm; as does that between manufacturing and services.

One hopeful sign for the U.S. economy would be continued stabilization in global manufacturing. Unlike in past cycles, since the U.S.-China trade war began, global manufacturing trends have been leading those in the United States; with optimism building around the benefits of global fiscal stimulus (more on that later in this report).

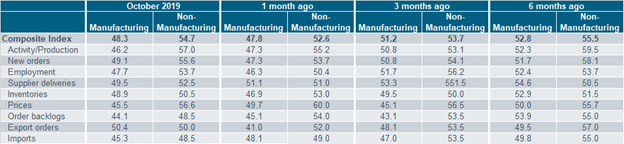

Included in the slew of recently-released economic data were the Institute for Supply Management’s (ISM) Manufacturing and Non-Manufacturing Indexes. Both measures ticked up in October, but the manufacturing sector still remains below 50 (which separates contraction from expansion). Despite the uptick, you can see from the table below that every component—except export orders, which surged in October—remains in contractionary territory. The same can’t be said for the services side, however, as the overall index stayed above 50 and bounced back from its fall in September—pulled up by nearly every component. A retrospective look at both indexes confirms that the services side has in fact remained in healthy shape, while manufacturing remains weak—no surprise given the stagnation in capital spending due to trade uncertainty. [To read more about the ongoing divergences in the economy, see Split Personality: U.S. Economy’s Bifurcation Persists].

Manufacturing Remains Under Pressure While Services Has Proven its Resiliency

Source: Charles Schwab, Bloomberg, Institute for Supply Management (ISM), as of 10/31/2019.

One strike with no outs

October’s payrolls report from the Bureau of Labor Statistics (BLS) was quite favorable, considering the lowered expectations due to the now-concluded General Motors (GM) strike. Notwithstanding the rather muted increase in average hourly earnings, which kept the year-over-year gain at a steady 3%, job creation was strong. The economy added 128k nonfarm payrolls with net upward revisions totaling 95k for the prior two months; and though the unemployment rate ticked up to 3.6% from 3.5%, it rose for the “right reason” in that the labor force participation rate rose. Our view has been that should the malaise in business/manufacturing start to morph into the consumer/services sides of the economy, the weakness will likely show up first in the employment channels. Based on still-low unemployment claims and healthy hiring data, we can say for now that the employment backdrop stands firm; although job openings have rolled over and bear watching.

Pause for effect

As expected, the Federal Open Market Committee (FOMC) cut rates by 25bps at the October meeting and lowered the interest rate on excess reserves (IOER) by 25bps. Most notable was the committee’s hint at shifting into pause mode for the foreseeable future, as Federal Reserve (Fed) Chair Jerome Powell dropped the pledge to “act as appropriate to sustain the expansion” from his press conference statement. Powell signaled that, going forward, the FOMC will monitor incoming data to assess whether further cuts are needed; as a strong labor market, solid job gains, and firm consumer spending have propped up the expansion.

As Liz Ann Sonders notes in her latest Fed commentary [Fed Cuts Rates as Expected … Three and Done or More to Come?], there have been eight interest rate cutting cycles since the early-1980s that have had three or more rate cuts. While past performance is no guarantee of future performance, in the years that the Fed had less than two cuts left after the third cut (1982, 1985, and 1988), there was no recession that followed and stocks performed quite well in the subsequent six months. Yet, in the five instances when the Fed had at least two cuts left after the third cut (1984, 1989, 1996, 2001, and 2007), stock market performance was poor. In fact, a recession ensued in three of the five years (1989, 2001, and 2007) with the Fed engaging in fairly aggressive easing cycles.

Fiscal stimulus emerging

Monetary policymakers at the Fed, European Central Bank (ECB) and Bank of Japan (BoJ) appear to be on hold heading into 2020 after lowering interest rates in 2019. The leaders of these central banks have made a concerted effort to ask fiscal policymakers to enact stimulus through stepped-up government spending or tax cuts—which have been made easier courtesy of low interest rates. There are some fresh signs that this may be unfolding.

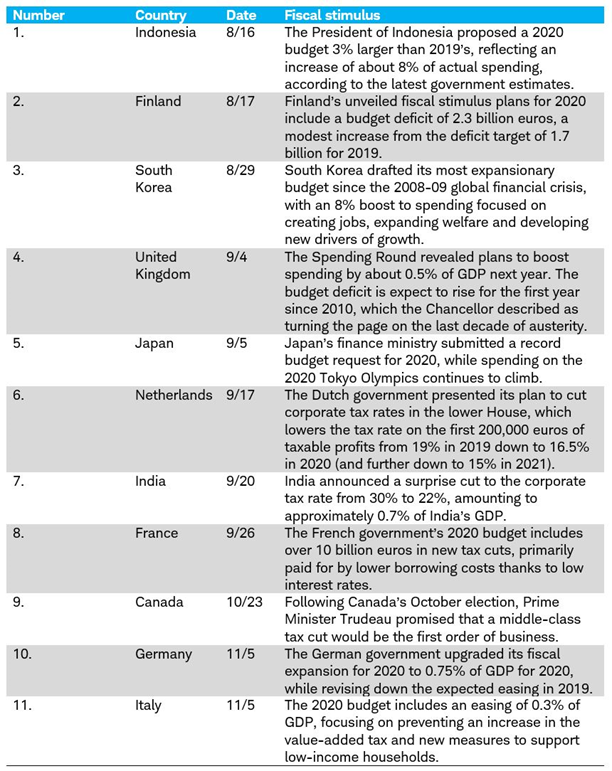

This week, Eurozone members submitted their 2020 budgets to the European Commission, revealing plans for new fiscal stimulus. These moves add to the growing list of countries focusing on fiscal stimulus; a phenomenon that started around this year’s annual August gathering of central bankers and finance ministers in Jackson Hole, Wyoming.

Global Central Banks Shifting to Fiscal Stimulus

Source: Charles Schwab

More fiscal stimulus could be forthcoming. Ahead of the November 10 elections in Spain, the Spanish budget has assumed no policy change except for previously-approved revaluations of pensions and the minimum wage, resulting in a fiscal easing of 0.1% in 2020. Yet this could change post-election and it may be the case in the United Kingdom as well. Following the U.K. election on December 12, new spending or tax measures may emerge, as both the Conservative and Labour parties have communicated intensions to do so.

This week’s budget submissions point to a potential overall fiscal boost of 0.3-0.4% in Eurozone GDP, which may ultimately translate into a faster 0.2-0.3% rate—given how spending impacts various growth channels. While these numbers may seem small, keep in mind that with economies like Germany reporting quarterly GDP growth of -0.1%, this boost could make the difference between a slowdown and a recession. Also, these estimates are not far from the estimated 0.3% effect on GDP from the United States’ 2018 tax cut, according to the nonpartisan Congressional Research Service (CRS). If more countries jump on the fiscal stimulus bandwagon, it may prove to be more effective than rate cuts at stimulating growth.

So what?

While volatility has remained subdued and U.S. stocks are at all-time highs, a near-term concern is that investor sentiment may be getting a bit too frothy. The potential signing of a “phase one” U.S.-China trade deal and rollback of some tariffs has contributed substantially to the rally; yet the proposals made have yet to be corroborated by anything in writing. Further, absent a trade deal that covers the major structural issues surrounding intellectual property (IP) theft, technology transfers, and supply chains, we find it difficult to envision a resurgence in corporate animal spirits and business investment—stabilization is more likely. Conversely, a positive shift in global growth may be in its infancy stages, as a more widespread adoption of fiscal stimulus may bode well for economies that have leaned too much on easier monetary policy. With many developments still at stake, we maintain our neutral stance on U.S. equities (with a bias toward large caps at the expense of small caps) and both developed and emerging market equities; and encourage investors to use volatility to rebalance and stay near their strategic asset allocations.

SOURCE:https://www.schwab.com/resource-center/insights/content/market-perspective