Lord Abbett: A Map Of The Equity Landscape At Mid-2022

A Map of the Equity Landscape at Mid-2022

Last month, leaders from across Lord Abbett’s global investment capabilities shared their views regarding the key challenges in the global investment and economic landscape at midyear—namely tightening monetary policy by central banks in response to surging inflation, recession fears, the war in Ukraine, and lockdowns in China that have exerted additional strains on the global energy and supply-chain complexes, among other topics. (Register to view a related webinar.) These challenges have contributed to the substantial financial-market volatility in the first half of 2022 and raise questions about how investors should adapt to market uncertainties arising from the unprecedented macro environment.

Beyond the macro outlook, what are the implications for specific asset classes? In the first installment of a two-part Market View, we surveyed Lord Abbett equity investment professionals for their views on key areas of the equity market and potential opportunities ahead. We will examine the outlook for major segments of the fixed-income market in the second part.

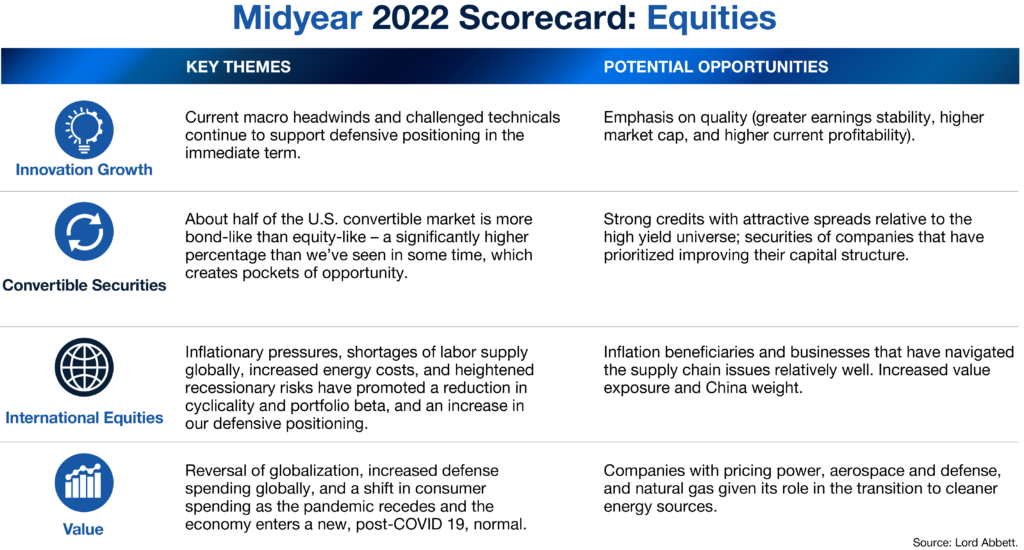

Innovation Growth Equities

In our view, key indicators for the market continue to support defensive positioning. Technical signals indicate the current challenges: inflation is too high; liquidity, as measured by central bank balance sheets, is now shrinking after steady expansion throughout 2020 and 2021; credit spreads have widened. And while corporate earnings have grown, we believe that earnings per share (EPS) estimates are more likely to be revised lower than higher in the months ahead. Of these key indicators, the dominant one, in our view, is inflation, as central bank efforts to combat inflation will almost certainly sow the seeds of a significant economic slowdown; already, higher prices and tighter financial conditions have cut demand in areas such as retail and housing. If we get relief on inflation, we believe the other metrics also cited should also improve. Until then, “don’t fight the Fed” and “don’t fight the tape”—that is, don’t place bets in the market that likely run against the tides of monetary policy and market technicals—are two simple concepts that may serve investors well.

Accordingly, we remain defensive with an emphasis on quality (loosely defined as companies with greater earnings stability, higher market capitalizations, and higher current profitability levels), with selective additions and overweights to our highest-conviction, high-growth names. Looking out beyond the immediate term, we believe the powerful secular forces that kept inflation low before the pandemic—namely demographics, high debt levels, and the technology revolution—will reassert themselves at some point to bring inflation down to more manageable levels, though the Fed’s 2% target appears a long way off. Tighter monetary and fiscal policy, too, should cause inflation to decelerate from very high levels. Furthermore, the technology revolution is ever more powerful with each passing year, providing a supportive backdrop for innovation in the consumer, communications, healthcare, and technology sectors in the decade ahead.

The opportunity set of attractive growth companies in these sectors—now at more reasonable valuations—continues to expand. Many of these companies have dominant market positions, are experiencing tremendous growth, are very early on in their penetration of their specific markets, and likely have years of high compounding annual growth ahead.

Convertible Securities

There have been several macroeconomic factors that have kept a lid on equity returns thus far in 2022. Perhaps most notably, inflation, in both quantitative data and qualitative comments from corporate management teams, has continued to temper investors’ near-term expectations for earnings growth. Alongside that, equity and fixed-income investors alike have had to price in significantly more monetary tightening than anyone expected at the beginning of the year—which has led to wider credit spreads. All these headwinds have created a challenging backdrop for convertible securities in 2022.

That said, we find convertibles attractive at current price levels, particularly those with lower equity sensitivity than the broader market. As of the end of June, close to half of the U.S. convertible market is more bond-like than equity-like—a significantly higher percentage than we’ve seen in some time. Many of the underlying stocks of these issuers have corrected significantly over the last year, but these companies have strong credit characteristics and enough time left before their convertible securities mature so that the embedded options (i.e., the opportunity to convert the bonds into common stock at the defined conversion price) can still deliver upside well above the stated yield-to-maturity on the bonds, in our view. We have also recently found some opportunities in companies that have worked to improve their capital structure— either through refinancing or buying back debt.

International Equities

In the first half of 2022, non-U.S. equities marginally outperformed U.S. equities. If we look under the hood, international growth equities considerably underperformed their value counterparts. Performance of markets outside the United States is often driven by many of the same factors that affect U.S. equity markets, and the first half of this year was no different, with red-hot inflation and a hawkish Fed having a meaningful impact.

Inflationary pressures created by the COVID-19 pandemic and the shortages of labor supply globally have been accentuated by the Russia-Ukraine conflict and its impact on supply chains and energy costs. Navigating through this environment has meant reducing cyclicality in international equity portfolios, as well as seeking out companies that might benefit from rising prices and businesses that have navigated supply-chain issues relatively well. Additionally, we believe the geopolitical conflict will have an enduring impact for businesses that will heighten the need for energy security, defense security, and supply-chain resilience. These themes are shaping our thought process around portfolio construction. Along those lines, we have increased our defense and energy exposure.

Inflation has been a major theme in recent quarters and remains a driver of our positioning. As higher inflation works its way into discount rates and corporate decision-making, growth stocks in non-U.S. equity markets are faced with headwinds, and value looks much better in comparison. Within value, financials, energy, and metals/mining were strong beneficiaries through the first quarter of the year. Since then, as the risks of recession and slowing global growth have grown, we have positioned more defensively. Within financials, there are two competing dynamics. On the one hand, higher rates should improve banks’ net interest margins. However, slowing economic growth poses risks of higher loan-loss provisions. As such, we reduced bank exposure in Europe, which we believe is at greatest risk of recession and an economic slowdown, and added to insurance companies and exchanges.

On the other hand, we have been adding to our China exposure. China has been struggling to meet growth targets due to its “Zero COVID” policy. Strict limits on mobility and frequent mass testing stemmed the spread of the virus and we believe the economy is primed for a reopening surge supported by strong fiscal spending and monetary easing. In addition, valuations have become far more attractive after increased pressure from Chinese regulatory authorities have contributed to a significant market rout over the last several quarters.

Value Equities

In the first half of the year, value significantly outperformed growth within U.S. markets as rates continued to climb, and investors gravitated toward what are perceived to be shorter-duration equities. Market sentiment shifted rapidly over the course of the second quarter from fears of extreme inflation, following the Russian invasion of Ukraine, to fears of recession in the wake of the U.S. Federal Reserve’s (Fed) decision to increase the pace of policy normalization in order to combat accelerating inflation. Following the shift in market focus, commodity-oriented areas of the market came under pressure in the back half of the second quarter. Within the energy sector, while we remain constructive on both capital discipline as well as capital return, we have taken profits across select exploration & production companies following the outperformance in the first half of the year.

As geopolitical risks heightened, supply chains were further disrupted, shining a light on the potential need for the reversal of globalization. More specifically, we anticipate that there will be substantial activity to rejuvenate oil and gas production outside of what may be perceived to be hostile areas. We believe this activity will benefit the oilfield services industry. Also, within energy, we have maintained our exposure to natural gas in light of tightening global supplies and natural gas’s role in the transition to cleaner energy sources. More broadly, we believe commodity prices will remain structurally higher over the medium term as supply chains are reconfigured globally to increase their resiliency. This trend was exacerbated by the Russian invasion of Ukraine. Another aspect of that conflict has been a greater emphasis on defense spending globally. We believe this will remain in place for some time and have increased our exposure to the aerospace and defense industry.

We continue to position our portfolios for a slowing economic environment as rates rise. Amid the flattening of the yield curve, rate volatility, and skepticism around global growth prospects, U.S. banks continue to come under pressure. In response, we trimmed our exposure to select banks. We have added to holdings within the insurance industry, which has exhibited pricing power; we expect the defensive appeal of this sector will increase if global growth begins to slow markedly.

As inflation indexes continue to come in near all-time highs, the strength of the U.S. consumer has come under question. While the lower-income consumer may face increasing pressure amid rising costs, we believe that there are still tailwinds in place, such as robust household balance sheets and a strong labor market. We would expect to see a rebound in consumer-oriented stocks if oil prices revert to more range-bound levels, and we are looking for opportunities within the beaten-down consumer sectors. Given ongoing inflationary pressures, we continue to seek out companies that maintain pricing power and exhibit elements of durability and resiliency. We do, however, remain skeptical of companies that we believe benefited from a pull-forward in demand stemming from the dislocations caused by COVID-19, particularly within the housing sector. As a result, we have pared back holdings of select housing-related stocks.

Looking ahead, we continue to look for companies with attractive quality metrics such as earnings stability. Durable businesses with robust free cash flows are of particular importance in this environment as these companies tend to have the ability to navigate increased market volatility.

Source: https://www.lordabbett.com/en-us/financial-advisor/insights/markets-and-economy/a-map-of-the-equity-landscape-at-mid-2022.html