Our Top Market Takeaways for September 16, 2022

Market update: Can’t take the heat

It was another week dominated by inflation, and markets felt the heat.

The higher-than-anticipated U.S. August CPI print (headline +0.6% MoM vs. consensus expectations of +0.3%) catalyzed the worst day of performance for the broad equity market since mid-2020 (when investors were first digesting news of the Delta variant). The S&P 500 fell more than 4% on Tuesday, with longer duration growth stocks tumbling more than 5%. Heading into Friday, stocks had erased last week’s gains.

The 2- and 5-year Treasury yields popped +34bps and +25bps to 3.90% and 3.68%, respectively, their highest levels since 2008, while the 10-year Treasury yield rose back to its highest level of the year (3.46%). The 2-year 30-year Treasury yield curve saw the most severe inversion since the Tech Bubble, Fed rate hike expectations for next week’s meeting climbed to 80bps (implying a ~20% probability of a 1.0% hike), and the U.S. dollar remains hovering at 20-year highs.

Against such a backdrop, we thought it would be helpful to consider some other volatile periods to see what lessons we could learn.

Spotlight: 5 things to consider when markets are volatile

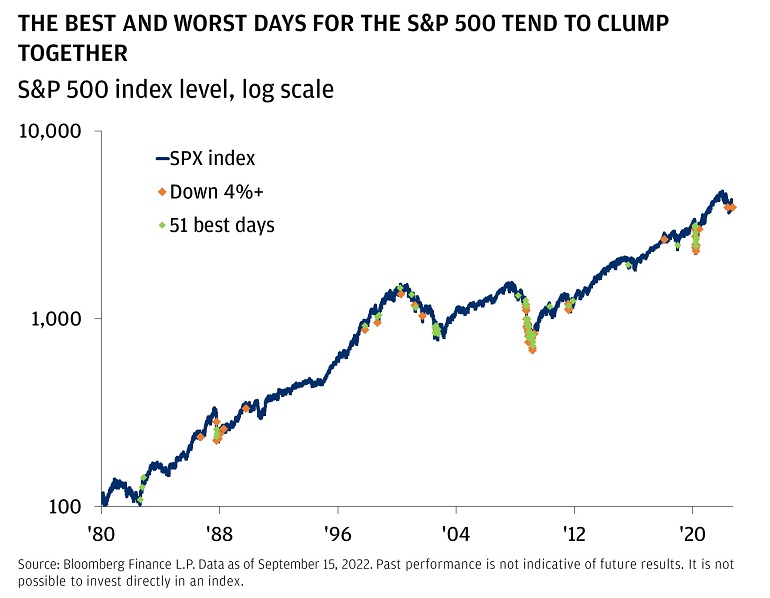

1. Big down days are tough, but staying invested is crucial. Since 1980, there have been 51 days during which the S&P 500 dropped more than 4% in a single session like they did on Tuesday (only 0.5% of the time). 21 of those days happened during the Global Financial Crisis in 2008/2009 and another 9 happened during 2020. After each instance, the market never failed to recover and make new highs.

If this week shook your confidence in staying invested, remember the potential cost of getting out of the market. In the past 20 years alone, the S&P 500 annualized 9.7%, but missing just 10 of the market’s best days, which tend to occur within less than one month of the 10 worst days, would have reduced that annualized return to 5.5%.

2. Don’t miss the forest for the trees. Short-term returns for portfolios aren’t great. Over the last year, a 60/40 portfolio of US stocks and bonds is down -12.4%. Over the last 2 years, that portfolio is up 5.8% (2.9% annualized). However, over the last 3, 5, and 10 years, the annualized returns are 6.2%, 7.3%, and 8.4%, respectively. The present era of high inflation and aggressive central bank tightening cycle is taking a toll, but the long term track record is strong – we expect diversified portfolios to continue that trend going forward.

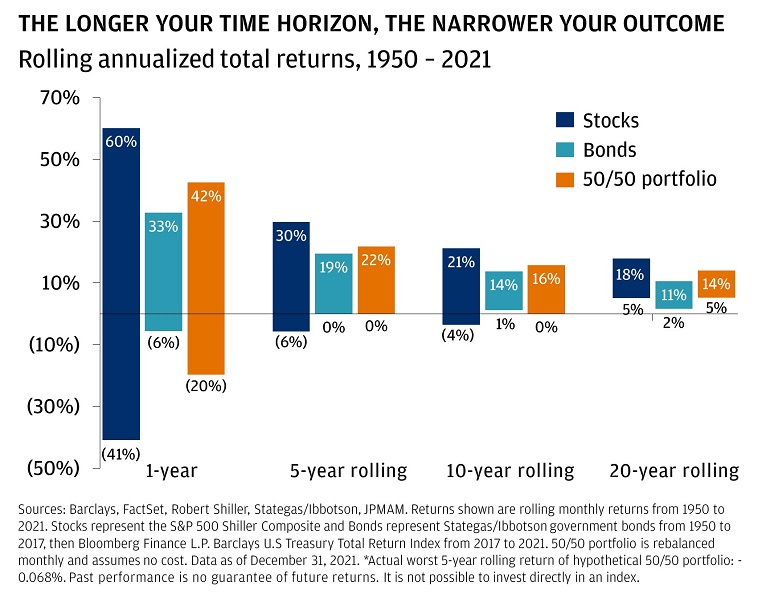

3. Understand the power of a diversified portfolio invested over the long run. While markets have bad days, weeks, and even years, history suggests that you are less likely to suffer losses over longer periods – especially in a diversified portfolio. While rolling 12-month stock returns have varied widely since 1950 (from +60% to -41%), a 50/50 blend of stocks and bonds has not suffered a negative annualized return over any five-year rolling period in the past 70 years. Historically, the longer you stay invested, the more certain you can be about the range of outcomes.

4. Time flies when you’re climbing back to highs. Goals-based multi-asset portfolios are meant to achieve financial goals through bull markets, bear markets, high volatility environments, low volatility environments, inflationary environments, deflationary environments, expansions, recessions, wars, pandemics, and anything else short of the heat death of the universe.

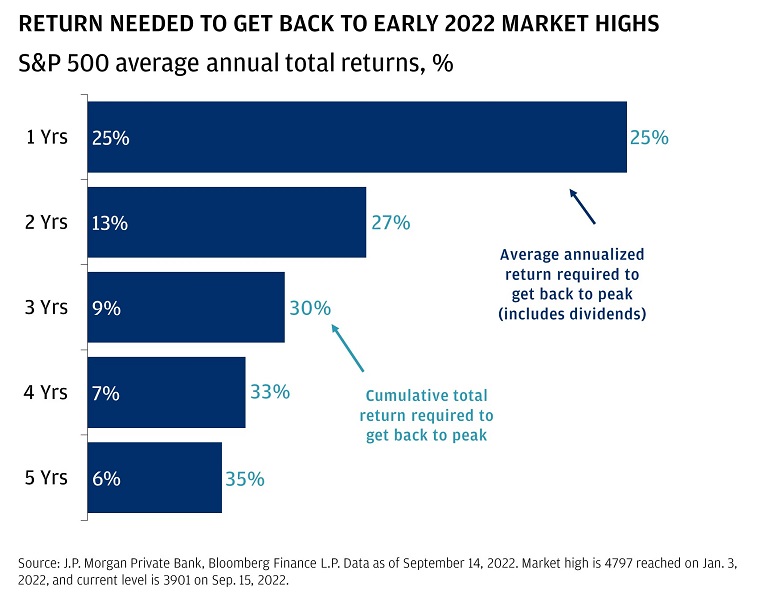

With investor sentiment near all-time lows, the previous S&P 500’s all-time high (~4,800 in early January) seems like a distant memory. But this too shall pass. From current levels, the market needs a ~25% return to get back to previous highs. Even if it takes 3 or 4 years, the average annual return needed, 9% or 7% respectively, would be right around historical norms.

5. Find value in murky waters. Through all of the daily volatility in markets and uncertainty in economic data, our objective is to build portfolios that allow investors to reach their goals with appropriate risk. It’s worth highlighting two opportunities that are offering compelling entry points.

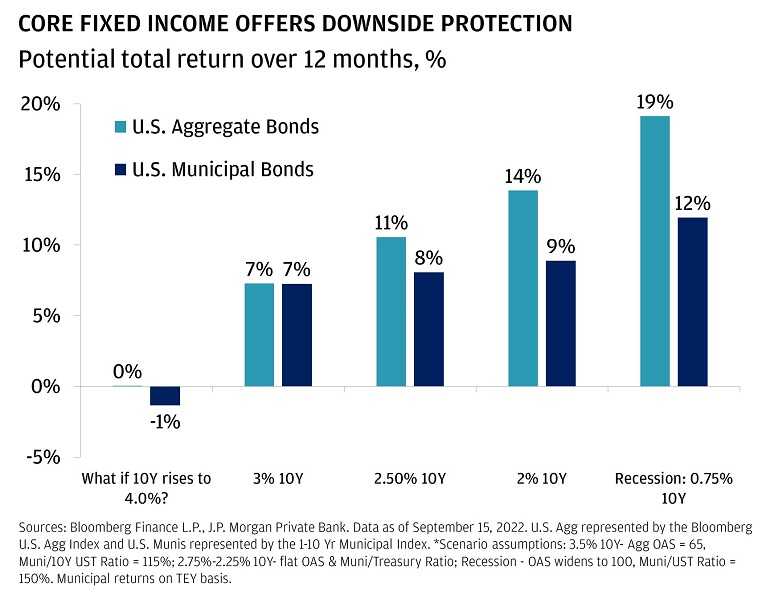

For one, core fixed income is our highest conviction idea that looks set to provide a buffer against potentially adverse economic outcomes. In the event that a U.S. recession does materialize and the 10-year Treasury yield ticks down from ~3.50% to 2.50%, we’d expect U.S. investment grade bonds to return ~11%. If instead the 10-year Treasury rises to ~4%, U.S. investment grade bonds would be flat.

In equities, we are making sure that we have a proper balance between sector, style, and size with a tilt towards defensive and quality companies. Meanwhile, mid cap equities, are presenting an interesting opportunity. Current valuations are well below their long-term average, compensating investors for a ~25% decline in forward earnings expectations – during the Great Financial Crisis, forward earnings estimates declined by 35%. Most of their revenue is derived from the U.S., a value-add in a world of European energy and Chinese property sector crises. And finally, history shows a track record of faster earnings growth rates and exposure to stronger capital expenditures from large cap companies.

In turbulent times, it is key to remember your core investing principles and consider capitalizing on windows of opportunity that the market presents. Please reach out to your JPMorgan advisor to hear more about how any of these dynamics may impact your plan.