Charles Schwab: Investors May Get Some Good News For A Change

November 29, 2018

Key Points

- Ominous signs for the world economy may be causing stocks to price in an imminent global recession.

- However, plunging oil prices, negative third quarter GDP growth in major economies and the decline in the global manufacturing PMI appear to be isolated, short-term events that already show signs of stabilization.

- Growth may rebound in the near-term and offer some relief for stocks.

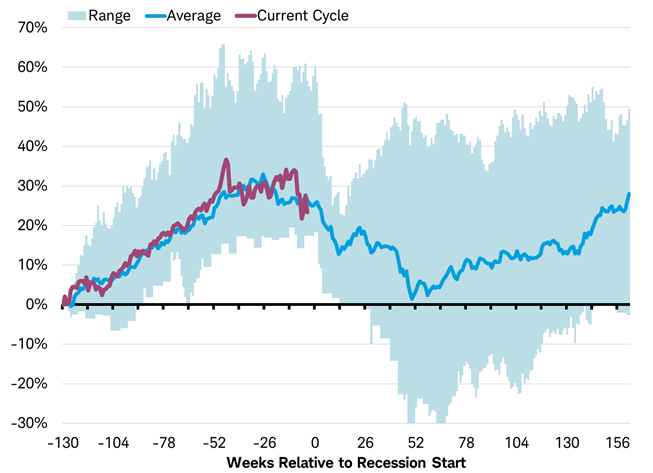

Has a global recession already begun? The past two months have seen plunging oil prices, several major economies reporting negative GDP for the third quarter, and the widely-watched global composite purchasing managers’ index slide from this year’s high down more than halfway towards 50, which marks the threshold level between growth and contraction. These ominous signs for the world economy may be causing stocks to begin to price in an imminent global recession, as you can see in the chart below.

Performance of MSCI World Index ahead of past 6 global recessions

Performance measured from 130 weeks before start of recession.

Source: Charles Schwab, Factset data as of 11/21/2018. Past performance is no guarantee of future results.

While a slowdown in global economic growth may be underway and there is heightened risk of a recession in the next 6-18 months, we may see growth rebound in the near-term and offer some relief to stocks. Let’s take a look at each of these ominous signs that may be impacting the stock market.

Oil’s plunge

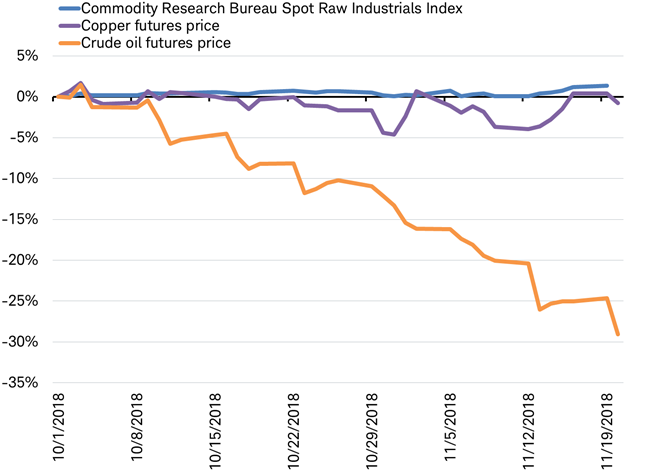

Commodity prices can be a signal of global economic activity; when prices fall it suggests a slowdown in production. This makes the plunge of nearly 30% seen in crude oil prices since the start of the fourth quarter potentially worrisome. However, declines have not been echoed in other economically-sensitive commodities like copper or even more broadly in the index of raw industrial commodities, the Commodity Research Bureau Raw Industrial Index.

Most commodities not joining in oil plunge

Source: Charles Schwab, Bloomberg data as of 11/21/2018. Past performance is no guarantee of future performance.

This suggests the drop is oil is largely driven by the rise in the supply of oil rather than worries over falling demand.

Negative GDP growth

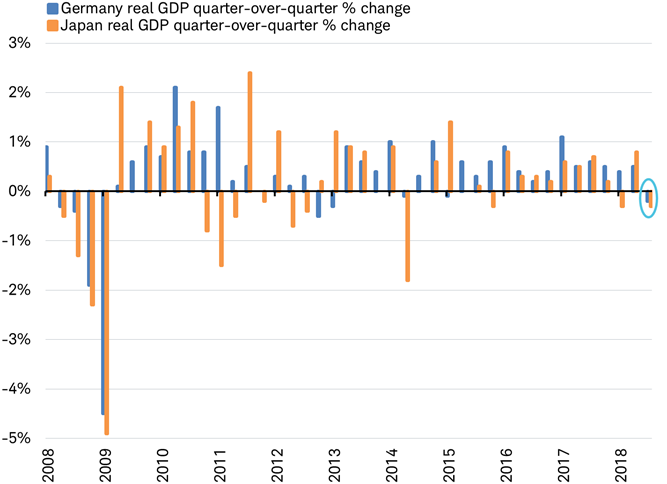

The economies of Germany and Japan contracted in the third quarter. Since they are the third and fourth largest economies in the world, when they shrink it can have a big impact on the global economy.

Third quarter GDP contracted for Germany and Japan, but may rebound in fourth quarter

Source: Charles Schwab, Bloomberg data as of 11/21/2018.

Germany reported a contraction in GDP of -0.2% (or -0.8% in annualized terms) for the third quarter. The weakness in real GDP was largely due to a contraction in industrial output as new vehicle emissions standards disrupted auto output. Data from the German carmakers’ association known as VDA (Verband Der Automobilindustrie E.V.) showed that September production plunged 24% compared with a year earlier. Also, inflation surged in September on higher energy prices, reducing inflation-adjusted GDP. Those headwinds have reversed in the fourth quarter, so real GDP in the fourth quarter is likely to rebound—the consensus estimate of economists is 0.5% (or 2% annualized growth).

Japan’s real GDP annualized contraction of -1.2% in the third quarter was largely due to extreme weather conditions and earthquakes combined with higher energy prices. Japan’s economic data has already showed a recovery from the string of natural disasters. The consensus of economists’ is forecasting a rebound to 1.9% GDP growth for the fourth quarter. The combination of slowing inflation, high business confidence, stabilization in China’s pace of growth, and the ramping up of construction ahead of the 2020 Tokyo Olympics should support growth.

Speaking of China, the second largest economy also showed some signs of weakness in the third quarter. While China’s pace of growth is far from recession, it slowed more than anticipated in the third quarter in lagged response to higher interest rates, restrained credit issuance, a stronger currency and trade tensions. The slower growth prompted policymakers to apply stimulus: cutting rates and weakening the currency. Any breakthrough or cooling of trade tensions could also help. If the pace of growth in China stabilizes, it should help support global growth.

PMI slide

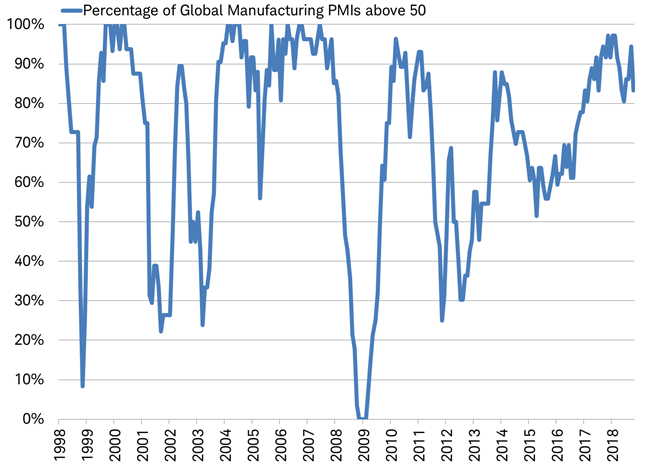

The purchasing managers’ index (PMI) is a timely indicator of the trend in the economy and is based on monthly surveys of companies tracking variables such as output, new orders, stock levels, employment and prices. The global manufacturing PMI, which combines all of the surveys from around the world, has fallen from this year’s high more than halfway to the level of 50, which marks the threshold between growth and contraction. The momentum and pace of the decline may be worrying investors.

However, this may be a normal adjustment after the PMI showed unsustainable strength earlier this year. At the start of this year, 97% of countries had a composite PMI above 50—the highest percentage during this global business cycle, as you can see in the chart below.

2018 began with 97% of countries having a PMI above 50; more than 80% still do

Source: Charles Schwab, Factset data as of 11/21/2018.

The breadth and strength of growth in the global economy is unlikely to be sustained throughout the year, but that doesn’t mean a recession is imminent. While the global PMI has declined, more than 80% of countries remain above 50, signaling continued economic growth.

Near-term relief

The growth scare may soon fade. If these indicators of global growth rebound or stabilize in the near-term, rather than continue to weaken, it may provide some near-term relief for stocks that lately seem to be pricing in an imminent recession.

Source: https://www.schwab.com/resource-center/insights/content/investors-may-get-some-good-news-change