Alliance Bernstein: Searching For Symptoms Of Three Mounting Risks

Global equities advanced in the second quarter, but the path was rocky. Incoming earnings reports will provide important clues about how companies are coping with mounting challenges—from trade wars to global growth—and how investors should position.

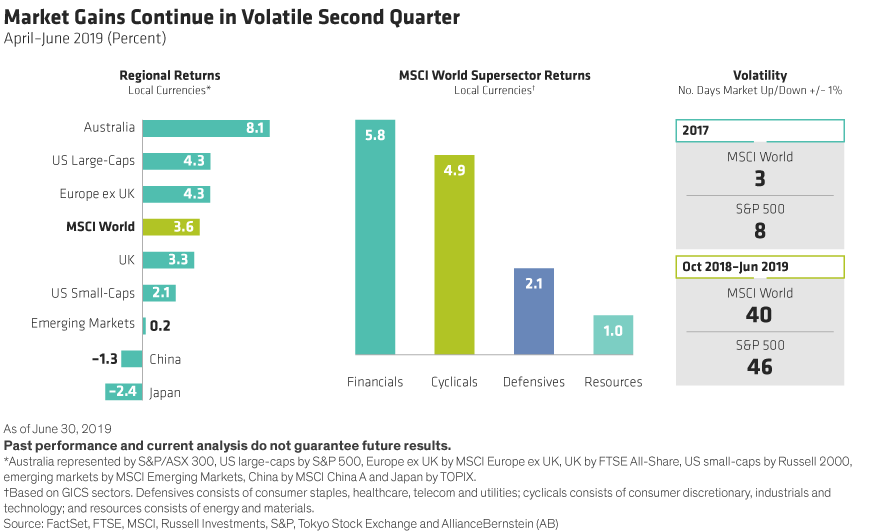

US and European stocks outperformed, while stocks in Japan and China declined (Display). Financials and cyclicals led the gains. Value stocks trailed growth stocks. The MSCI World Index ended the quarter up 3.6% and has surged 16.7% in the first half of the year, in local-currency terms.

Why Are Markets So Volatile?

Despite the solid first-half gains, performance patterns were unsteady. Four months of strong gains in early 2019 were disrupted by sharp May declines, as trade fears resurfaced to dominate market sentiment. Markets have been volatile since the fourth quarter of 2018 (Display above, right); during three of the past nine months, global equities posted sharp declines.

Recent volatility reflects growing concerns that the global economy is in its late-cycle stages after a decade of steady growth. Yet this cycle has several unusual features. The pace of GDP growth has been modest. Even after a series of Fed hikes, interest rates are extremely low and unlikely to rise soon, given renewed central bank pledges to maintain loose monetary policies. On the other hand, rising populism is threatening to unravel decades of globalization and trade integration, with unpredictable consequences for companies and stocks.

Against this backdrop, financial markets are delivering mixed signals to investors. While equities reach new heights, low bond yields—with the 10-year US Treasury yield at about 2.0% and the yield curve inverted at times—reflect pessimism about the outlook. However, yields are being suppressed, in part, by continued aggressive liquidity measures by central bankers, particularly in Europe and Asia.

Three Sets of Investing Risks

With uncertainty high, our analysts and portfolio managers are paying particular attention to three types of risks today: policy risk, macroeconomic (cyclical) risk and interest-rate risk. Second-quarter-earnings season, beginning this month, will provide important indications about how companies are adjusting.

+ Policy Risk—the US-China trade dispute is making it extremely hard for companies to invest for the future. As hopes of a deal rise and fall, investors should pay attention not just to what CEOs say but to what they do, particularly in terms of investment. Companies that express optimism but aren’t investing should ring alarm bells; those that reduce capital expenditures too much could impair their future growth paths. We’re looking for companies that show a thoughtful balance of managing uncertainty with long-term investment needs.

Trade concerns go beyond the obvious tariff victims. Supply chains in autos and technology deserve special attention, as companies located at key links of manufacturing processes may provide early signs of trade-war fallout.

Beyond trade wars, political risk is heightened in other sectors. We’re monitoring political rhetoric around US healthcare reform, as legislative changes could impact drug prices and insurers’ profitability. In Europe, the growing risk that Britain might exit the European Union without a deal is forcing many UK and European companies to make contingency plans for a potential shock.

In the technology sector, last year’s spending boost, fueled by President Trump’s tax reform, has largely dissipated. And growing regulatory scrutiny of tech and new media giants means that tech companies must demonstrate resilient sources of revenue and earnings growth.

+ Macroeconomic Risk—global growth is likely to remain sluggish. As the second-quarter-earnings season begins, certain cyclical sectors, such as autos and financials, can provide early intelligence about macroeconomic trends. After several years of very low levels of loan losses, we’re closely watching bank reports for any signs of a deteriorating credit environment.

In retail-oriented industries, sales trends can help identify pockets of weakness. Conversely, companies showing solid sales in a tougher economic environment may possess pricing power, which is a significant sign of resilience in industries vulnerable to a cyclical downturn. Advertising spending is also a harbinger of weakness in corporate sentiment; when companies start feeling the pinch, ad spend is often one of the first budget items to be cut.

+ Interest-Rate Risk—while markets watch interest rates for signs about the economy and the relative attractiveness of equities, banks feel the impact of rate movements more directly. In the first quarter, bank executives warned that net interest margins—the difference between what banks pay for deposits and charge for loans—could get squeezed, as deposit costs were likely to rise along with rates and increased competition. Now, with rates falling again, banks may struggle to charge more for loans, which will hit their interest income. Those that can continue to generate loan growth may be better placed to weather this margin pressure.

In the short term, lower-rates-for-longer could provide relief for companies that borrowed heavily in recent years. But keep your on eye on the balance sheet—lower rates are no excuse for a company to take excessive leverage, especially in a world of weakening growth.

How to Stay Invested

Despite these risks, we think there are good reasons to stay invested in stocks. Corporate earnings are strong, and equity valuations, while not cheap, are not overly stretched either. Continued stimulus and suppressed interest rates should support equity gains—even if earnings growth moderates. What’s more, we haven’t seen the exuberance of previous cycles, when excesses in technology and subprime lending created unsustainable bubbles that wreaked havoc when they burst. So we don’t anticipate a market shock and we think equities can deliver moderate gains, though return patterns will be bumpier than in recent years.

Rather than trying to predict policy and macroeconomic outcomes, we believe investors should focus on neutralizing unpredictable risks. How? Fundamental and quantitative analysis can help steer a portfolio away from holdings that may be too exposed to arbitrary hazards. Research should also aim to identify companies that control their own destinies, benefit from resilient sources of noncyclical growth and are backed by experienced management teams that can navigate erratic conditions with confidence.

Sharon Fay is Head of Equities at AllianceBernstein

Christopher Hogbin is Chief Operating Officer of Equities at AllianceBernstein

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

Source: https://www.alliancebernstein.com/library/global-equities-searching-for-symptoms-of-three-mounting-risks.htm